Europe’s Chemical Sector Under Stress

A report shows that chemical plant closures in Europe surged sixfold since 2022, reaching a cumulative 37 million tons of chemicals capacity – or around 9% of European production capacity

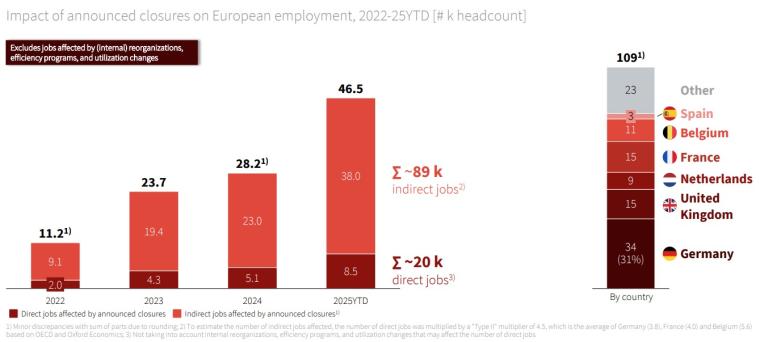

Since 2022, chemical plant closures in Europe have increased sixfold, resulting in the loss of 37 million tons of capacity—about 9% of the continent’s production output—and costing 20,000 direct jobs. According to a study named the European Chemical Closures & Investments Radar 2022–2025 conducted by Roland Berger, and commissioned by the European Chemical Industry Council (CEFIC), a further 89,000 indirect jobs are at risk due to the industry's vital position in Europe's value chains.

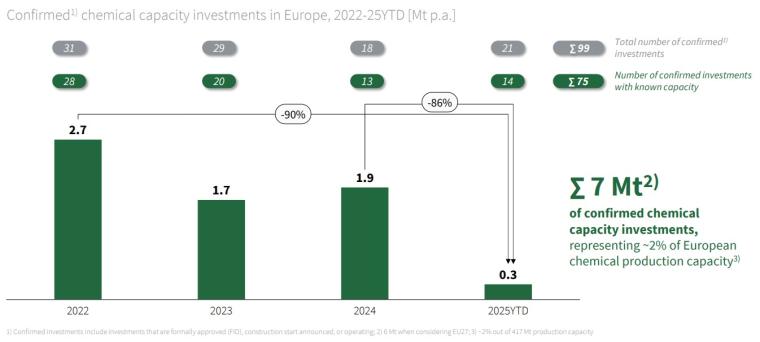

The report also reveals a sharp slowdown in new investments, highlighting growing concerns over the competitiveness and long-term viability of Europe’s chemical sector. Annual announced investment capacity fell from 2.7 million tons in 2022 to just 300,000 tons in 2025, amounting to approximately 7 million tons in total over 2022–2025. This drop reflects a shift from broad investment across multiple innovation pathways—like electrification, hydrogen feedstocks, and circular plastics – to barely one pilot initiative.

With closures now significantly outpacing new investments, the European chemical industry is contracting. This trend points to deepening uncertainty for the sector and raises serious questions about Europe’s ability to maintain a competitive, resilient industrial base.

Marco Mensink, CEFIC’s Director General said: “It’s no longer a question of being five minutes before or after twelve. The sector is under severe stress and breaking. The rate of closures has doubled in a year, and even worse, annual investments are half and close to zero. On both sides, the speed is accelerating, not slowing. We need decisive action this year, with impact at factory floor level.”

CEFIC is now launching a systematic, recurring tracker of chemical plant closures and investments as a key performance indicator (KPI) for European competitiveness and policy effectiveness In January 2025, CEFIC published its study on the Competitiveness of the European Chemical industry, identifying 11 million tons of announced capacity closures across 2023-2024 in the EU27.

Roland Berger was commissioned by CEFIC to report this KPI in independent Radar reports. This first report covers announcements made between Jan. 1, 2022 and Dec. 8, 2025 , with updates following several times a year. The following executive summary gives an overview of the current report’s key findings.

Closures

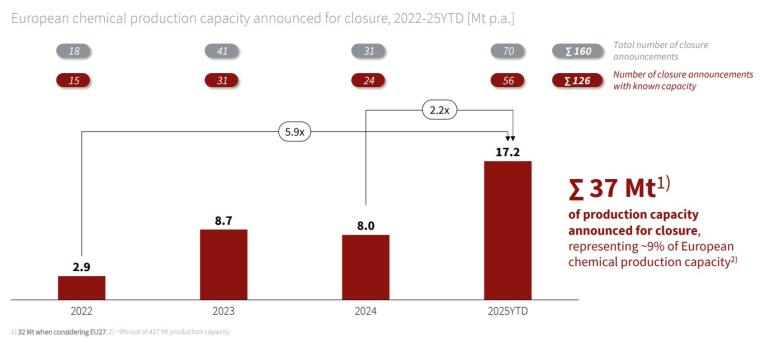

Between 2022 and late 2025, announced closures in the European chemical industry increased sixfold from 2.9 million tons to 17.2 million tons per year, and doubled between 2024-25, totaling 37 million tons in 2022-25 and representing about 9% of the European chemical production capacity.

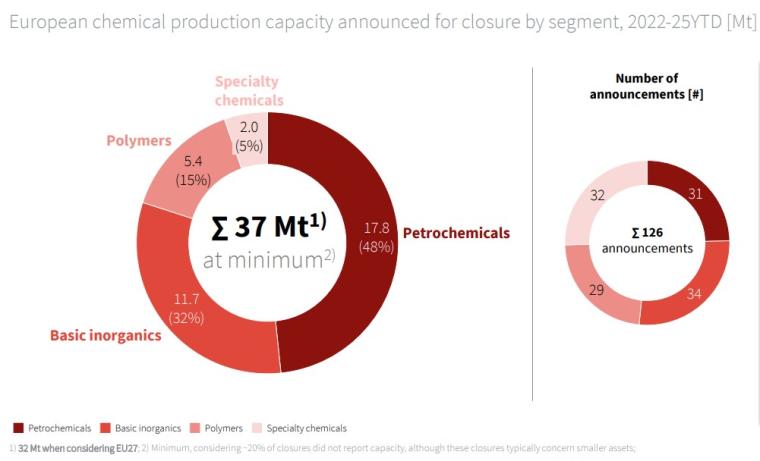

These capacity closure announcements have been made mainly within upstream petrochemicals (17.8 million tons, 48%), followed by basic inorganics (11.7 million tons, 32%), polymers (5.4 million tons, 15%), and specialty chemicals (2.0 million tons, 5%). The number of announcements is more evenly split between segments.

Within petrochemicals, about 50% of the total announced capacity closures concern nine steam crackers which corresponds to a 16% net reduction in European steam cracking capacity, all located in integrated chemical clusters, putting these clusters under increasing pressure.

Closure announcements span across Europe, with the largest shares in key chemical industry countries including Germany (8.8 million tons, 25%), the Netherlands (7.2 million tons, 20%), UK (4.5 million tons, 12%), France (3.9 million tons, 10%), Italy (2.5 million tons, 7%), Belgium (2.3 million tons, 6%), Spain (1.6 million tons, 4%) and the rest of Europe (6.0 million tons, 16%).

Across these countries, about 20,000 direct jobs are cited to be affected.

In 49% of the cases, companies indicate energy cost competitiveness as the primary rationale for closing, followed by demand-related considerations (19%), overcapacity (9%), and regulatory factors (8%).

Investments

Confirmed investments on the other hand follow a decelerating trend, from 2.7 million tons in 2022 to 0.3 million tons in 2025 including a -86% decrease over the last year, totaling 7 million tons over 2022-25 and representing about 2% of the European chemical capacity production capacity.

Petrochemicals is the main segment with 3.8 million tons (59%) of confirmed investments in 2022-25, which only partially offsets the -17.8 million tons closures.

The largest confirmed capacity investments are in Belgium (2.4 million tons, 36%), Germany (0.8 million tons, 12%), and France (0.4 million tons, 6%), accounting for about 60% of the total.

Similarly, confirmed investment CAPEX has decreased by a factor of five from EUR 7.6 billion in 2022 to EUR 1.5 billion in 2025 – Germany (EUR 1.4 billion, 10%) is below France (EUR 1.7 billion, 12%) and the Netherlands (EUR 1.5 billion, 11%) despite having Europe's largest chemical industry.

Investment themes include projects related to the battery value chain (EUR 1.9 billion, 14%), emission reduction (EUR 1.9 billion, 14%), and recycling (EUR 1.5 billion, 11%) although, these themes follow the overall decreasing trend.

Net Effect

Considering both announced closures and confirmed investments over 2022-25, there is a growing asymmetry potentially leading to a net capacity reduction of -30.2 million tons – This asymmetry could be understated, as investments typically have longer time horizons (2-5 years) while closures are nearer-term (1-2 years).

Countries with the largest number of closures are not those attracting the main investments, resulting in a growing imbalance in key countries including Germany (-8.0 million tons), the Netherlands (-6.9 million tons), UK (-4.2 million tons), France (-3.5 million tons) and Central and Eastern Europe (-3.4 million tons) – Belgium as the exception, has a relatively neutral balance (+0.1 million tons), related to a selection of relatively large projects.

Segments most affected by closures are not seeing similar levels of investments, resulting in an imbalance in the upstream petrochemicals (-14.0 million tons), followed by basic inorganics (-11.3 million tons) and polymers (-4.8 million tons) segment, whereas specialty chemicals show a more balanced outcome (-0.3 million tons), supported by investments in the battery value chain.