Global Competitiveness of EU Chemicals Sector

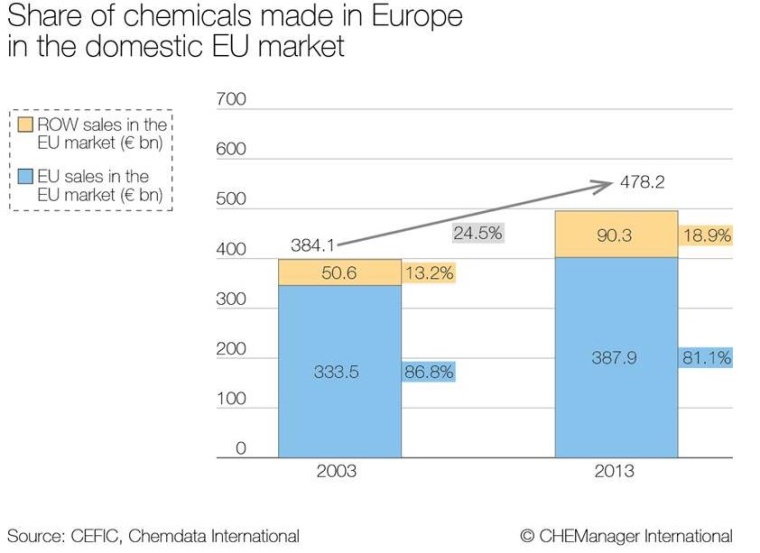

Domestic EU market share

The European chemical industry, with sales of €527 billion (2013), is one of the largest industrial sectors in the EU. Despite the apparent strength of the industry, the current situation gives cause for concern. The global chemicals market doubled in the period 2003-2013. Europe has participated in this global growth, with chemical sales steadily rising in absolute terms in the past decade. However, due to stronger relative growth in other parts of the world, the EU's share of global sales decreased significantly over the period (from 32% in 1993 to 17% in 2013). What is worrying is the decline in domestic market share over the past ten years (Fig. 1).

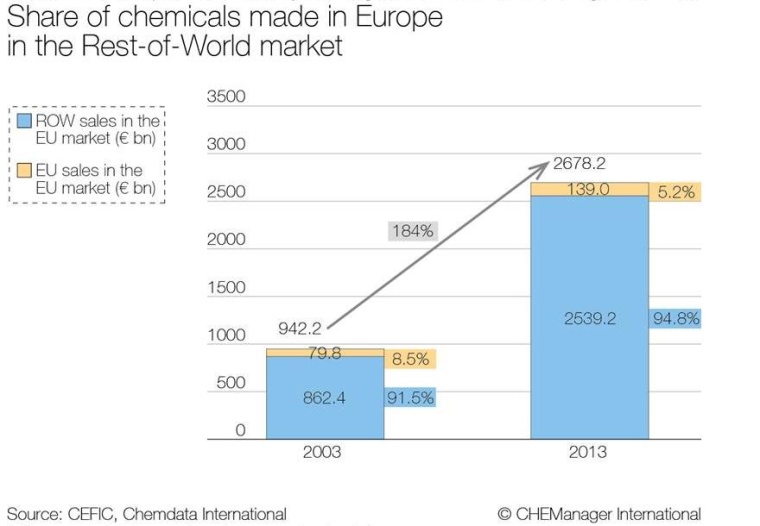

Rest-of-World market share

In addition, the European chemical industry, which is an exporting industry, with one-quarter of its production being exported outside the EU, is also losing share in the Rest-of-the World market (Fig. 2). The key question is therefore whether the decline in global share is entirely due to the "growth rates" effect or is the sector also losing competitiveness? In order to have a systematic approach to estimating the competitiveness of Europe, CEFIC commissioned Oxford Economics to analyse the situation. The study confirms that the greater part of the decrease in export market share observed over the past 20 years is due to declining competitiveness.

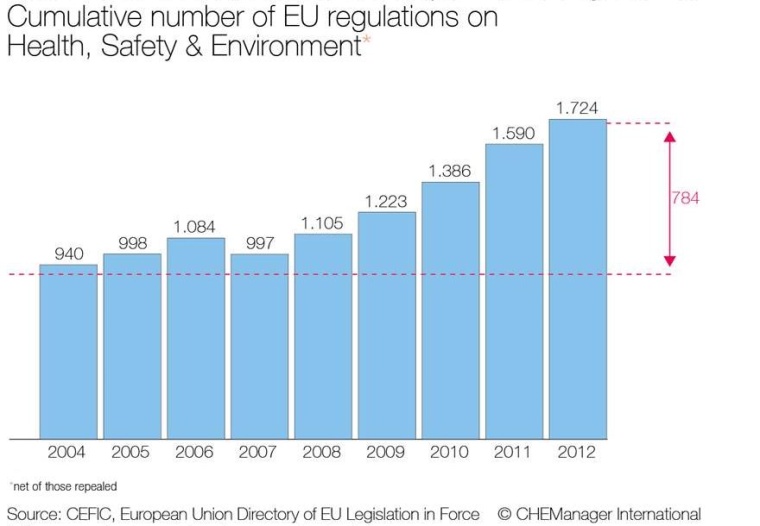

Costs of implementing legislation

The analysis revealed several potential causes for this loss in market share. One important factor cited by companies as affecting competitiveness is the growing cumulative costs of implementing European legislation in the chemical sector. Fig. 3 reveals the cumulative number of EU regulations on Health, Safety & Environment repealed since 2004. This takes both personnel and capital resources away from innovation and production and into regulatory compliance, which clearly reduces the competitiveness of the European industry compared with other regions. Disadvantaged energy and feedstock prices are another clear disabler of competitiveness.

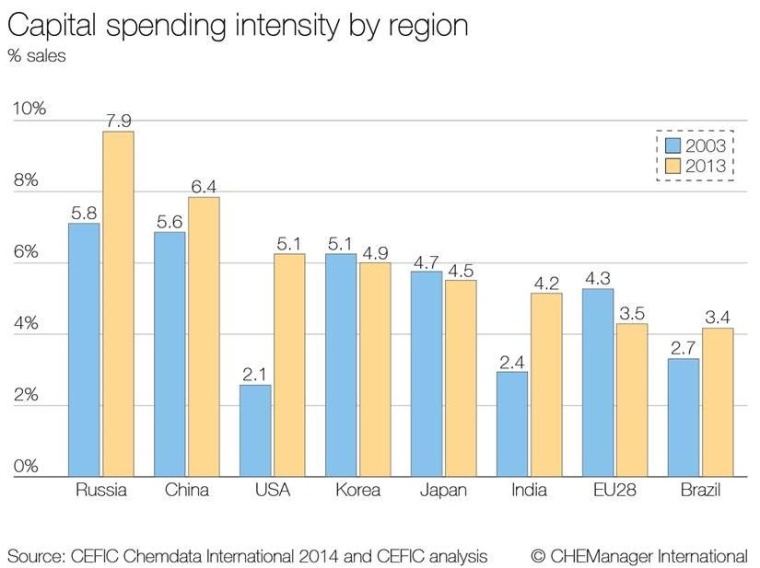

Comparison of capital spending intensity

A clear indicator is the cost of producing ethylene, the highest volume building block in the chemical industry. Making ethylene in Europe is about three times more expensive than in the US (due to the shale gas boom) or the Middle East. This is boosting profits abroad and attracting billions of dollars in investment. The more investment the more competitive the region becomes and vice versa. In the EU we see declining levels of capital spending intensity compared with other regions (Fig. 4). For example, the US (with nearly 200 chemical investment projects totaling nearly $130 billion) and the BRIC countries remain the key targets of chemical investment.

most read

Novo Nordisk to Cut 9,000 Jobs Globally in Major Restructuring

Novo Nordisk announced a global workforce reduction of approximately 9,000 positions to streamline operations and reinvest DKK 8 billion (€1 billion) in growth opportunities for diabetes and obesity treatments.

VCI Welcomes US-EU Customs Deal

The German Chemical Industry Association (VCI) welcomes the fact that Ursula von der Leyen, President of the European Commission, and US President Donald Trump have averted the danger of a trade war for the time being.

Dow to Shut Down Three Upstream European Assets

Building on the April 2025 announcement, Dow will take actions across its three operating segments to support European profitability, resulting in the closure of sites in Germany and the UK.

Orion Announced Plans to Shut Down Carbon Black Plants

Carbon black manufacturer Orion Engineered Carbons plans to rationalize production lines in North and South America and EMEA.