China’s rising salaries improve Europe’s competitiveness

Implications of the Closing Wage Gap between European and Chinese Chemical Industries

-

Dr. Kai Pflug, CEO, Management Consulting — Chemicals, Hong Kong, China

Dr. Kai Pflug, CEO, Management Consulting — Chemicals, Hong Kong, China -

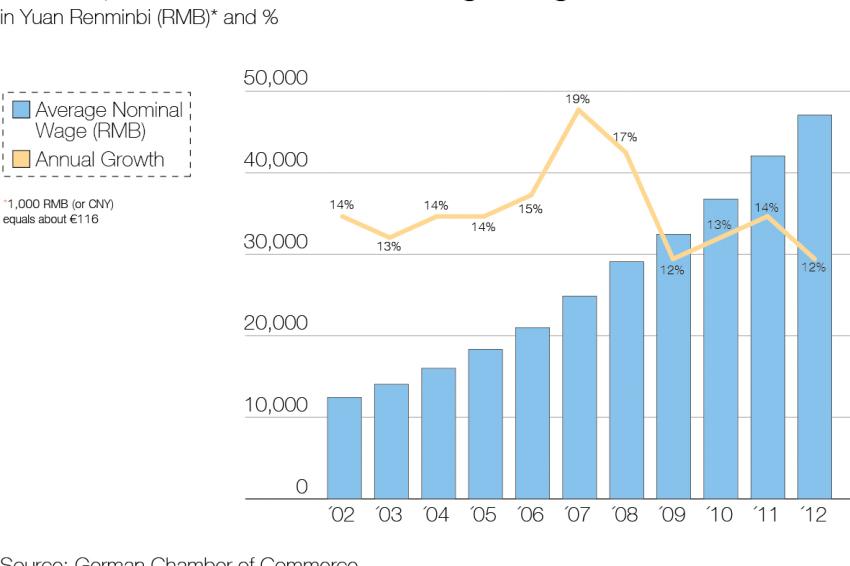

Fig 1: Development of Chinese average wage in Yuan Renminbi (RMB) and %. 1,000 RMB (or CNY) equals about € 116. Source: German Chamber of Commerce, China calculations based on Chinese National Bureau of Statistics

Fig 1: Development of Chinese average wage in Yuan Renminbi (RMB) and %. 1,000 RMB (or CNY) equals about € 116. Source: German Chamber of Commerce, China calculations based on Chinese National Bureau of Statistics -

© apops - Fotolia.com

© apops - Fotolia.com

Variety of Factors Influence Salaries - In the last 10 years, salaries in China have been rising at an average annual rate of about 14%. Though this rate has recently been somewhat lower, it is still around 10%. At the same time, salaries in Europe have increased at well below 3% per year. As a result, the salary gap between China and Europe has decreased quite substantially. Of course, this also applies to the chemical industry.

This does not mean that salaries in China have already reached European levels, at least with regard to the positions requiring lower levels of education. Blue-collar chemical workers in China may receive monthly salaries of €300-€500 - still substantially below their European counterparts. On the other hand, for experienced sales managers in the chemical industry, the monthly Chinese salary may already reach a base salary between €4,000 and €7,000.

Factors Influencing Wage Differences

Obviously the wage gap between the Chinese and the European chemical industries depends on a number of factors. An important one is the region within China. For example, the minimum wage in Shanghai is about 60% higher than the one in Guizhou, a poor province in western China, and though the specific minimum-wage values are not particularly relevant for the chemical industry, they can be seen as an indicator of the overall wage level in a province. Thus Beijing and Shanghai have wages that are much closer to European levels than those of some of the western provinces.

Another factor is the position level. Generally, the wage gap between Europe and China is much bigger for lower-level positions - an expression of the higher level of inequality of Chinese society.

Finally, there is some difference based on the ownership type of Chinese companies. While the wage level of listed Chinese companies is similar to that of Western-owned companies, wage levels are still somewhat lower for state-owned companies and private companies. As a consequence, the salary gap to the European chemical industry is bigger for the latter.

The main reason for the large salary increases is the overall increase in gross domestic product rather than the increase of salaries relative to GDP. In fact, private consumption - which is linked to salaries - accounts for a comparatively small and stagnating share of Chinese GDP compared with Europe. Other reasons are the slightly decreasing overall working population and the government policy to frequently increase minimum wages (by up to 20% per year).

However, the biggest driver for salary increases is still the lack of relevant experience within the labor force. China's economy has grown so much in the past decade that not enough people have the technical and management experience required, particularly for the higher-level positions. Thus competition for these highly qualified employees is fierce, and companies need to pay competitive salaries to hire them.

A final aspect that should not be forgotten when discussing the salary gap in the chemical industry is an indirect effect. Most segments of the chemical industry are not particularly labor intensive. This reduces the direct effect of rising wages. However, chemical industry segments may still be strongly affected if their customer industries are labor intensive. For example, producers of textile chemicals in China may in the long run be affected as their textile-producing customers move to lower-wage countries such as Bangladesh or Vietnam.

How Chemical Companies React

There are many ways companies can react to rising salary levels. Perhaps it is most interesting to see which of these measures chemical companies so far have not used much.

Western chemical companies have not reduced staff. In fact, staff numbers at Western companies still increase at a rate of 5%-10% per year. This is despite the occasional reduction. For example, BASF had a staff of about 7,800 in greater China at the end of 2011, then reduced this number by about 500 employees one year later but increased again to more than 8,400 employees at the end of 2013. In general, for each chemical company reducing its employee number, there are still several late entrants into the Chinese market hiring additional staff.

Also, companies have not substantially moved away from China. Unlike the effect of high labor cost on labor-intensive chemical segments in the European chemical industry (e.g., fine chemicals), so far no shift toward lower-cost countries has occurred. The main reason is the necessity to produce where the market is: in China. In addition, countries with lower wages do not have the infrastructure and educational level to justify the shift for the comparatively low-labor intensive chemical industry.

Thirdly, while chemical companies have tried to reduce further salary increases, they have only had moderate success so far. Past routine annual increases of 10%-12% have been replaced by a more moderate 7%-8% in the past one or two years, but the general upward trend has not been stopped.

In contrast, chemical companies in China strongly focus on increasing the productivity of their workforce. This includes a variety of measures such as:

- Increased automation and general improvement of work processes

- Increased capacity utilization, e.g., by widening the locally produced portfolio (to achieve a dilution of salary costs on higher total sales) - this trend has been in line with the general move toward localization of production

- Widening the qualification of the workforce, and extending its tasks - for example, some chemical companies have trained the electricians in the afternoon and night shifts to also take over operator duties, thus reducing the number of staff present during these shifts

- Increasing the retention of employees in order to improve the overall experience of staff in their positions, e.g., via active employer branding

According to Chinese statistics and some third-party surveys, the productivity increases thus achieved are roughly in line with salary increases, which makes the rising wages more palpable for the chemical industry.

Outsourcing of selected functions is another tool utilized particularly by foreign companies. While most companies still feel somewhat uncomfortable outsourcing production of chemicals (unlike in Europe, where toll production is more common), the bigger use of third-party distributors, as a way of outsourcing part of the sales function, is getting more frequent. This particularly holds true for those companies that have already created strong own sales teams in China and are now re-evaluating the use of this own staff for smaller, lower-value customers.

Increased flexibility of pay is employed in order to limit pay increases to the actual improvement of company results. Private local chemical companies use this tool to a large extent, often offering quite low base salaries and a huge upside potential based on personal results, particularly for sales staff. Chinese companies also accept a much wider wage differential, paying quite low wages for employees deemed easily replaceable (e.g., accountants) while highly rewarding their star performers, e.g., in sales.

An action taken primarily by local Chinese companies has been to shift part of their production away from the expensive tier 1 cities in eastern China, and toward western and central China. This can indeed result in substantial savings in wage payments; however, it also brings additional issues such as scarcity of qualified staff in these regions and inferior infrastructure, particularly for companies involved in import and export. These issues have so far kept most foreign companies from considering a move away from the main chemical centers in coastal China.

What This Means

Generally, although management of chemical companies in China is highly aware of the substantial salary increases, the issue is still not perceived as very severe. The times when China was mostly a cheap production site for export elsewhere are long gone. Within the next few years, China will be the biggest chemicals market in the world. Thus there is no real alternative to having a strong China presence and consequently to hiring and paying qualified staff. Therefore the closing salary gap is unlikely to have a significant influence on the chemical industry in China.

Contact

Managm. Consult. Chemicals

RM1302, 13/F CRE Bldg.

Wanchai, Hong Kong

China

+86 1368 1873992