APIs in China

Pharma Industry Booming in Asia

-

© mark huls - Fotolia.com

© mark huls - Fotolia.com -

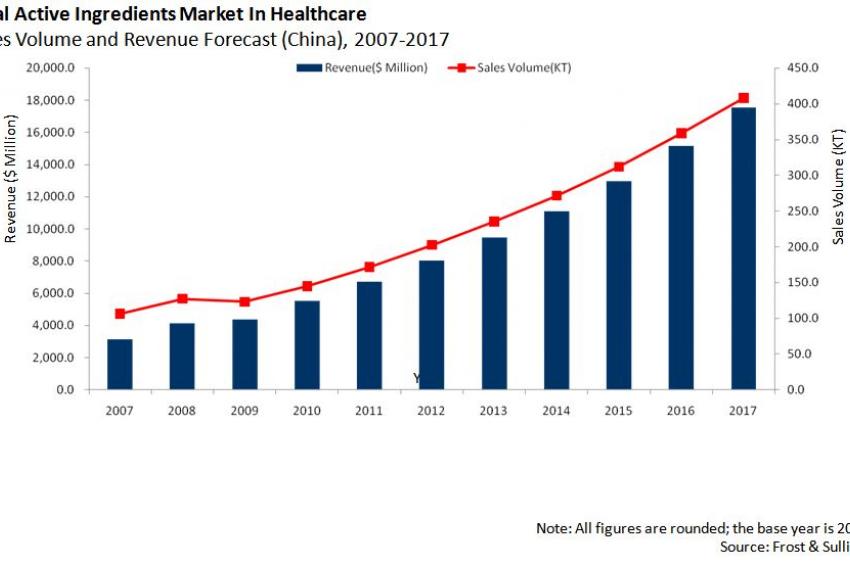

Figure 1

Figure 1 -

Figure 2

Figure 2

Pharma in China - The Chinese pharmaceutical market is one of the largest due to the large size of its population. As the basis of pharmaceutical industry, the API market offers great growth opportunities for manufacturers both in-house and overseas. The API segment makes up more than 50% of the export value of China's pharmaceutical trade.

As a result, the Chinese market for APIs is rapidly growing and is estimated to witness a compound annual growth rate (CAGR) of 18%from 2010 to 2017. Ingredient suppliers in the Chinese API market will be keenly following the events in the pharmaceuticals industry, which is in the midst of integration. Apart from the sustained and rapid growth of the pharmaceuticals industry, the long-term use of multiple specialized drugs for an ageing population and the reform of the Chinese medical system have also given a shot in the arm to the Chinese API market.

As drug administrations in China put more effort into the supervision of the pharmaceutical industry, safety and environmental protection issues have become the areas of concern for the API producers. API producers in China are required to follow the guidelines such as the good manufacturing practice (GMP), which was revised by the Ministry of Health of the People's Republic of China in 2010. These manufacturers are also required to reach higher levels of standards and certifications, which are similar to the Japanese and European standards.

Chemical API Segment will Continue to Dominate the API Market in China

Chemical APIs are produced through conventional routes of synthesis. They are extensively used in many therapeutic segments such as cardiovascular, central nervous system disorder, oncology, gastrointestinal, etc.

The wide usage in these applications ensures the stable growth of the chemical API market. Chemical APIs have historically dominated the global API market, and this situation is reflected in the Chinese market. China is the world's second largest producer and exporter of chemical APIs, with competitive advantage mainly in antibiotics, vitamins, antipyretics and analgesics, etc. The growth of the market is mainly driven by sustained growth in chemical drugs, especially the generic sector.

Continuing patent expiries over the next few years is also considered to be a key driver for the demand of chemical APIs. By 2012, about $80 billion of patented drugs (including drugs for tumor, cardiovascular disorders and digestive problems) are expected to go off-patent, which will lead to great growth opportunities for the Chinese API market.

The generic chemical API segment is considered to be well-positioned to seize these opportunities. The chemical API segment added the largest portion of sales volume with 95.1% of the total market sales volume in 2010 due to the large consumption volume of chemical drugs.

Although declining in market share, the chemical API segment will continue to dominate the API market in China in the next few years. Key competitors in this segment include CSPC Pharma, NCPC, Northeast Pharmaceutical Group and other foreign and local companies.

Focus on Biotech APIs is Next Highlight of API Industry in China

Biotech APIs refer to APIs produced through the biotech routes of synthesis. Main categories of biotech APIs include amino acids, polypeptides, proteins, enzymes and others. The key product portfolio of Chinese biotech APIs includes heparin, hyaluronic acid, chondroitin sulfate, urokinase, coenzyme A and others.

Biopharmaceuticals are effective in treating certain complex diseases such as tumor, diabetes, and other immune related diseases with fewer side effects. The advancements in biotechnology and the ongoing research of biosimilars are expected to create great potential for growth of the API market globally. Comparing to chemical APIs, biotech APIs accounted for a negligible market share.

However, this segment is facing a strong growth potential at a rate of 20%, which is higher than the overall API market in China. Furthermore, the generic biotech API sector is expected to grow faster than the innovative API sector. The share of the biotech API segment is expected to increase in the next few years due to the increasing focus on biological drugs.

The Chinese biotech API market is an emerging market and is also highly fragmented. Driven by the healthcare reform in China, Chinese ingredient manufacturers have made efforts for developing biotech APIs. High profit margins and competitive price of biosimilars comparing with innovative APIs also make it attractive for API companies.

More leading API manufacturers are stepping into the biotech API segment in order to tap the growth potential in this market. Some of these manufacturers have the capacity to compete with foreign pharmaceutical companies in certain segments like heparin products, which are used for antithrombotic therapy. Competition in the biotech API segment is currently lower due to the complex biotech routes of synthesis.

Providing a Cost-Effective Solution to the Customers

The API market in China is highly fragmented with many participants involved. Companies located in Hebei province, Shandong province and the Northeastern areas of China are mostly large state-owned enterprises, while rising API production bases in Suzhou and Zhejiang provinces have a strong advantage in export markets. Key competitors in the Chinese API market include CSPC Pharma, NCPC, Zhejiang Medicine, Anhui BBCA Biochemical, Northeast Pharmaceutical Group.

The suppliers range from CMOs (contract manufacturing organizations) of innovative and generic APIs (for example Hisun Pharmaceutical, focusing on antibiotics and antitumors), to many other suppliers which provide mainly bulk APIs with low profit margins. As more and more foreign companies established capacities in China to transfer the costs and environmental pressures, local API suppliers are facing greater competition.

Price fluctuations in 2010 have affected the revenue growth of the Chinese API market. Currently, high-performance-cost ratio products are the key strengths of Chinese API suppliers. Several China-made products have played a major part in the international market. In the long term, prices are expected to rise due to the general rise in price of raw pharmaceutical ingredients and government policies which are pushing the upgrading of the industry.

Some of the pharmaceutical companies are vertically integrated to manufacture their own pharmaceutical formulations. The vertical integration is expected to help these companies to reduce costs and control the supply channel of raw materials. As the integration trend of the Chinese pharmaceutical industry is revealed, market concentration gets higher for both the generic and innovative API segment. Customers tend to build long-term relationships with ingredients suppliers. Thus, new entrants of the market are facing challenges to strive for customers.

While the potential for growth of the API market is huge, overcapacity for bulk products is greatly reducing the profitability of the API manufacturers and traders, which is mainly due to over investment. The low-margin generic API products such as vitamins and some of the antibiotics accounted for the majority of the total API market in China.

For instance, the proposed capacity of vitamin C, a representative of bulk products, is expected to be more than 200 kilo tons, which will be far more than the global demand of this product. Ingredient suppliers can offset the issue of expanding production capacities by adjusting their product portfolios in line with consumer trends to maintain the profit margin. They can also achieve higher profits by focusing on the biotech API segment, which holds considerable potential, but currently accounts for a negligible share of the market.

Contact

Frost & Sullivan

Clemensstr. 9

60487 Frankfurt

Germany

+49 69 7703343

+49 69 234566