Navigating the Future of Chemical Distribution

Key Industry Trends and Strategic Imperatives that Shape the Sector

-

The future of chemical distribution will be shaped by distributors who successfully deploy their value-adding capabilities to navigate an uncertain market environment. | © Grispb - stock.adobe.com

The future of chemical distribution will be shaped by distributors who successfully deploy their value-adding capabilities to navigate an uncertain market environment. | © Grispb - stock.adobe.com

In 2024, the chemical distribution industry is at a pivotal moment, navigating both challenges and new opportunities. As distributors grapple with a landscape shaped by shifting global trade routes, demand constraints, and digital disruption, their roles are evolving far beyond traditional bulk breaking. Going forward, distributors are positioning themselves as critical value-added partners, vital to the success of the global supply chain.

This article highlights current industry trends and strategic imperatives that will shape the future role of ‘next level distribution’.

Understanding the Current Market Context of the Chemical Distribution Industry

Circling back to 2023, five core beliefs were articulated by The Boston Consulting Group regarding the future of chemical distribution: an expected market softness in the short-term before growth picks up again at ~2.5% CAGR, increased reliance on outsourcing by principals, the diversification of distributor portfolios, the rising importance of performance delivery, and the increasing emphasis on value-added services. While the decline in demand and revenues, particularly in Europe, was more severe than expected over the past year, these beliefs still largely hold true. However, the context in which distributors operate in 2024 has changed.

In recent years, the chemical market has experienced significant upheaval. Prior to the pandemic, the industry enjoyed steady demand, globally intact supply chains, and predictable growth. Chemical distributors acted as general partners for the longtail. However, the combination of Covid-19 supply chain disruptions, prolonged destocking and unsustainably high margins elevated the position of chemical distributors and fundamentally altered the paradigms under which the industry operates.

Today, players along the chemicals value chain are operating in a ‘new normal’. In Europe, regulatory scrutiny, high energy costs and inflation have eroded competitive advantages and placed a squeeze on margins, prompting many companies to rethink sourcing strategies. Geopolitical uncertainties, environmental challenges, deglobalization trends and protectionist policies are reshaping the business landscape further, pushing many toward more localized or regional supply chains. As a result, principals have increasingly turned to distributors, not only for the long-tail, but mor and more also the mid-tail and application-specific services to ease their P&Ls.

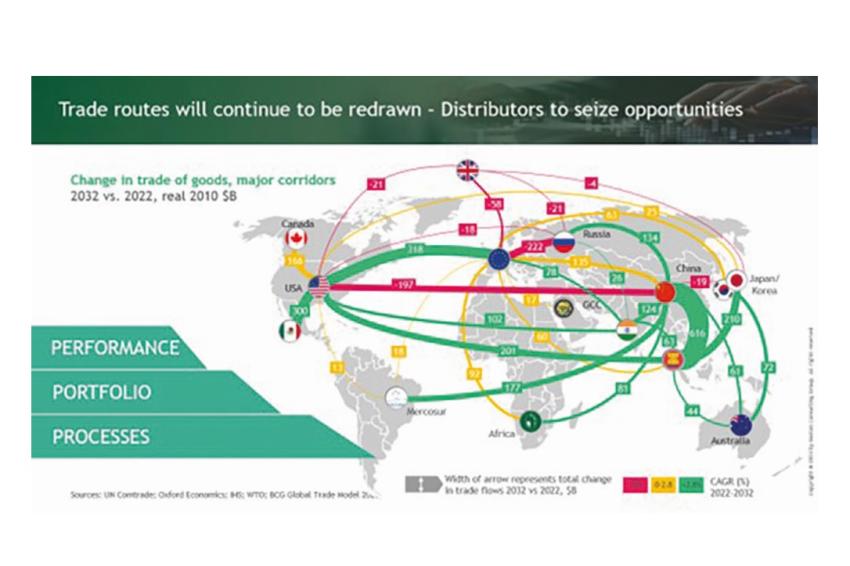

In addition, the global trade landscape is expected to undergo significant changes, reshaping competitive dynamics for principals and distributors as projected until 2032. Amongst others, a further decoupling and de-risking of key international trade relationships, particularly between the US and China, as well as Europe and Russia is expected. While these shifts introduce new challenges, they also open up new growth opportunities in emerging markets such as Southeast Asia, Latin America, and Africa. Moderate growth is expected between the EU and Africa, while trade between the US and Mexico, and China and ASEAN, is projected to experience robust growth. Regionalization of trade will be a major focus area.

“Regionalization of trade will

be a major focus area.”

As global trade routes shift, distributors must rethink their supply chain strategies and their role, leveraging new opportunities and new principals in these (emerging) markets to maintain their competitive edge.

Navigating this multipolar world will require flexibility and strategic thinking. ‘Next-level chemical distributors’ will need to take three key actions to ensure success:

1. Performance through

Digital Capabilities

Digitalization is a pivotal enabler of performance improvement in chemical distribution, forming the foundation for growth and efficiency. Digital tools and platforms will be essential for driving top-line growth and cost efficiency, enabling distributors to respond more effectively to market changes. Distributors who have invested early in building digital capabilities are now reaping measurable benefits, with leading companies reporting gains of 2–5 percentage points in gross profit margins and 1.5–3 percentage points in EBITDA margins vs. laggards.

For distributors still in the early stages of digital transformation, now is an ideal time to build capabilities that will not only enhance their digital muscle but also align with evolving market demands. With advanced technologies, digital tools, and service providers more accessible than ever, distributors can focus on platforms, AI, and automation to boost their performance significantly — at greater speed of transformation.

2. Align Portfolio with Future Market Demands

Distributors need to reassess their portfolios, focusing on building relationships with suppliers that align with future market demands while evaluating their value-added services and capabilities. In this regard, mergers and acquisitions (M&A) will remain crucial for strengthening distributors’ portfolios, while they should simultaneously conduct a thorough evaluation of which elements to exclude from their future offerings that will not act as a key differentiator for them.

M&A activity is expected to have reached new heights by the end of 2024 with 35+ deals by the top 50 global distributors, particularly in regions like Asia-Pacific and Latin America. Analyzing the strategic intent of those acquisitions, more than 50% have focused on expanding regional reach, while 30% concentrated on expanding application breadth.

Beyond regional expansion and portfolio diversification as the main strategic rationale for M&A, deals are increasingly focused on enhancing supply chain and service capabilities. Distributors are looking to acquire infrastructure, such as transport hubs and application-specific services, that can help them build more resilient supply chains and improve service quality.

Additionally, strategic partnerships are becoming a critical enabler of growth, particularly in areas like AI, sustainability, and customer experience — especially for those companies who cannot or do not want to host specific capabilities in-house through targeted M&A. In fact, over the past 18 months, there is an increase in announced alliances of >20%. By leveraging these strategic partnerships, distributors further differentiate their portfolios.

3. Optimize Core Processes with AI

Finally, the advent of generative artificial intelligence (GenAI) opens new opportunities for efficiency and effectiveness increases. Over 70% of chemical distributors have started to experiment with GenAI, both in front-end and back-end applications, yet, full-scale deployment is pending. In specific instances, AI is already empowering distributors to deliver more personalized interactions by identifying customer patterns and prioritizing leads through predictive insights. However, distributors ought to focus on deploying AI on a large scale to realize its full potential and optimize their core processes, from forecasting, sales and operations planning (S&OP), and inventory management to route optimization and sales acceleration. This is when the investments into GenAI will positively influence the P&L and distributors can achieve substantial cost savings and operational efficiency, securing a lasting competitive advantage.

Strategic Imperatives for the Future

As the chemical distribution industry continues to evolve, three key strategic imperatives have emerged as critical to long-term success:

Monetize digital investments: Distributors must focus on converting their digital investments into measurable performance improvements. Digital tools can help distributors drive cost efficiency, improve service levels, and maintain a competitive edge in an increasingly crowded market.

Future-proof the portfolio: Distributors need to ensure that their portfolios align with future market demands — in terms of their principals, product and services portfolio. M&A and strategic partnerships will continue to be a key strategy for portfolio enhancement. At the same time, distributors should take a hard look at what will not be part of their future portfolio.

Leverage AI to optimize core processes: AI offers the potential to revolutionize core processes, but it must be deployed at scale in core processes to unlock its full value. Distributors must move beyond isolated experiments and integrate AI across all operational areas, to drive efficiency and scalability.

The future of chemical distribution will be shaped by distributors who successfully deploy their value-adding capabilities to navigate an uncertain market environment.

Madjar Navah, Managing Director and Partner, BCG, Dusseldorf, Germany

Tobias Mahnke, a Managing Director and Partner, BCG, Munich, Germany

Adam Rothman, a Managing Director and Partner, BCG, Chicago, USA

-

Fig. 1: The context is changing – shift from supply to demand constraints. | © BCG

Fig. 1: The context is changing – shift from supply to demand constraints. | © BCG -

Fig. 2: Trade routes will continue to be redrawn — distributors to seize opportunities. © BCG

Fig. 2: Trade routes will continue to be redrawn — distributors to seize opportunities. © BCG -

Fig. 3: Portfolio — reasons for M&A to evolve, while strategic partnerships are on the rise. © BCG

Fig. 3: Portfolio — reasons for M&A to evolve, while strategic partnerships are on the rise. © BCG

-

Madjar Navah, BCG | © BCG

Madjar Navah, BCG | © BCG

-

Tobias Mahnke, BCG | © BCG

Tobias Mahnke, BCG | © BCG

-

Adam Rothman, BCG | © BCG

Adam Rothman, BCG | © BCG