Global Specialty Chemicals is a World of Extremes

Getting Ahead in a Janus-Faced Market

-

Specialty chemicals has evolved to be a world of extremes – dominated by larger players and offset by the more traditional focused and multi-business smaller cap specialty players.

Specialty chemicals has evolved to be a world of extremes – dominated by larger players and offset by the more traditional focused and multi-business smaller cap specialty players. -

Uwe Nickel, Arthur D. Little

Uwe Nickel, Arthur D. Little -

-

A Fragmented Industry - The global specialty chemicals industry has revenues in excess of $550 billion and is quite fragmented with 350 industry sub-segments and considerable geographic diversity. While the industry provided considerable growth and added value characteristics through the early 1990s, it has been on the path of commoditization for over a decade.

The economic crisis that peaked in 2009 featured a significant decline of revenues in North America and Europe but comparatively better performance among Asian specialty chemical sectors.

It has regained strength in the beginning of 2010 and has reached today all time highs with historically high earnings before interest, tax, depreciation and amortization (EBITDA) margins for nearly every specialty chemicals company due to excellent utilization rates and a partially regained strength to pass raw material prices to customers.

The world of specialty chemicals has evolved today to be a world of extremes - dominated by larger players or new larger entrants that lever diversified portfolios, scale and more sophisticated management approach, offset by the more traditional focused and multi-business smaller cap specialty players. The development in and after the economic crisis while having tested the robustness of both focused and larger diversified players has not driven the level of consolidation thought likely by many industry observers and has interestingly underscored the financial resiliency of this segment.

The industry shift to larger diversified portfolio structures and the commodity-light approach has been a theme that has been employed by many successful industry participants. The shift rightfully reflects a higher value financial path for these companies looking at sustained cash flow potential and asset intensity.

Big is Beautiful: Scale and Portfolio Diversification

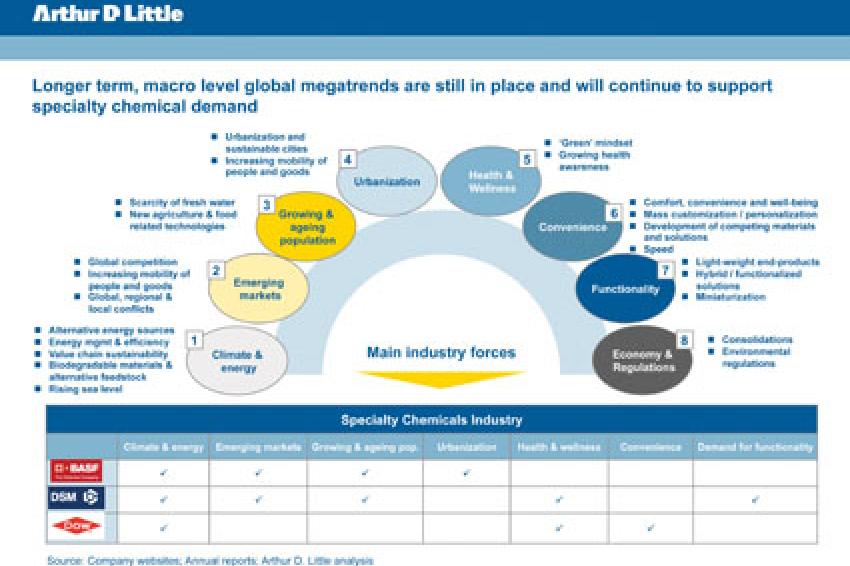

Increasingly today, the specialties market is becoming dominated by larger portfolio players with multi-chemical capability bringing management sophistication, scale and global reach. These sophisticated players are pursuing complex, multi-technology growth markets and platforms in nutrition, electronics and other attractive product areas that are supported by strong macro-level growth trends. These are large and long duration investments that also usually require acquisitive entry for at least in part. We have been seeing a range of acquisitions by companies like Dow, DSM and BASF over the years that are strategically motivated filling in the "mosaic" pieces that fit with longer-term strategic ambitions and increase entry barriers for smaller, less sophisticated players.

Consequently, following global megatrends and incorporating them into the strategic portfolio management as well as finding new growth through innovation provides large opportunities for the specialty chemicals industry if companies can leverage their capabilities and size. For small specialty chemicals companies it will be difficult to finance long-term innovations that help to solve the key challenges of humankind and generate the amount of profit in return.

China and the Middle East: Aggressive Growth in Specialties?

Asian companies currently have a ravenous appetite for cross-border deals to access more specialties growth to cover the rising need of specialties countries like China. The specialty sector in many ways is illusive to these new entrants - except, of course, to the more commoditized parts of the industry that have far lower entry barriers. Much of the specialty sector is rife with commercial complexity that includes a product technology and customer complexity dimension that present very significant barriers to easy entry.

The desire to grow in specialties and need to access intellectual capital will likely drive some additional cross border deals. These transactions will serve to provide an impetus to develop a more common view of return criteria and we believe are healthy for the normalization of the industry. A couple of large sophisticated players in China have emerged that will help consolidate the fragmented China market and build meaningful capability in specialties moving forward.

Furthermore, the Middle East - which has focused on base chemicals based on cheap feedstock rather than on the development of specialty chemicals over the last 25 years -will mainly boost itself through acquisitions or joint ventures. The search of opportunities in the specialty chemicals market (instead of more petrochemicals) as strategic portfolio alternatives has been triggered by changes in feedstock availability and prices.

This also goes for local or government-owned petrochemical companies that have to search more for alternative products and markets that create value through the process chain and a higher specialization rate via application services. On top of it, there is a clear demand in this region to increase the specific employment rate per ton produced (which is 10 to 50 times higher in specialty chemicals compared to petrochemicals) to contribute to the efforts and needs to overcome high unemployment rates in some of the Middle East countries.

David vs. Goliath: The Power of Focus

While larger portfolio players will have an edge in accessing more sophisticated growth opportunities, the power of focus is tried and true in the specialties area. Companies like Ecolab, IFF, Altana and Merck KGaA are small to medium and highly profitable companies that are leaders in their respective fields by focusing on a relatively narrow but highly specialized portfolio.

The value of focus extends through to market, domain and business model approach. These segments often have a significant incumbency advantage and nice entry barriers that are often not technology related, but rather related to fragmented market structure, branding and strong commercial innovation on the basis of excellent application know how and highly functionalized products.

While these examples are more extreme in terms of focus, there are many cases of companies that have created more focused businesses from larger diffuse portfolio - for example, Arch Chemical - the biocide company - and Albemarle with a leading position in catalysts and selected fine chemistries. In both cases, the companies created profitable niches in which they can build out advantaged positions.

Well-chosen specialty domains can be highly profitable and, if well managed, sustainable for advantage, and certainly defensible from many forms of new entry, but often times not scalable or providing much in terms of growth optionality.

Consolidation Path: Where's All the Consolidation?

There has been a fair amount of consolidation over the last few years that has been largely driven l by cross-border interests and larger strategic portfolio strategies. We have seen BASF aggressively pursue several sizeable transactions including Engelhard, Ciba and Cognis - addressing several strategic growth ambitions. Dow's acquisition of Rohm and Haas and Solvay's recent takeover of Rhodia has been an historic event in terms of the magnitude of the portfolio shift attempted.

While timing appeared to be the enemy of BASF's Ciba acquisition and Dow's purchase of Rohm and Haas lead to relatively high EBITDA multiples, it is a tribute to management have executed on these multi-step implementations in the middle of a downturn swing of the economy in 2008. Today, these acquisitions have become significant and profitable cornerstones of the portfolio of those companies going forward. The ultimate company will have a diverse specialties platform that should be positioned for success across an array of attractive growth markets, albeit this can only be accomplished with a price that makes it difficult for the deal to ever be accretive given the timing.

While a number of companies have escaped the distressed category in the past 12 months, new industry consolidation has been stymied by availability of credit, relative valuation levels and perceived risk related primarily to demand uncertainty.

It's All About Growth: Driven by Portfolio and Innovation Management

Ultimately, creating value is all about driving sustainable growth that can be attributed to strong portfolio and innovation management. The portfolio side incorporates the both the business and geographic aspects of portfolio management. Companies like PPG have done a great job of managing the geographic aspects of their portfolio and illustrate the value that can be garnered from optimizing along this dimension in the context of low growth portfolio. But the fullness of portfolio management requires proactivity to manage the underlying growth of a corporation's portfolio with the addition of corporate growth platforms that have linkage to the company and present attractive growth potential.

The other lever that companies have at their disposable to manage growth is innovation. But other than doing more of the same or incremental innovations is a strictly market-driven approach to get more to the unmet needs of consumers. Enhancement of improved products into new markets or even enlargement into new markets and new products and services will force the necessary step change. This can only be achieved by leaving the traditional paths of finding new growth and combine several innovation technologies to a new cocktail to find new spaces or the "needle in the haystack" of a traditional market.

By facing the changes of the specialty chemicals markets and taking rigorous actions to focus or diversify on a very large scale, top management will be able to leverage the performance and turn it into sustainability going forward.

Contact

Arthur D. Little GmbH

Gustav-Stresemann-Ring 1

65189 Wiesbaden

Germany

+49 611 7148 0

+49 611 7148 290