Pharma Sourcing from India and China

26.01.2011 -

-

India and China continue to be the chosen destinations for a pharmal industry hungry to lower research, development and manufacturing costs without sacrificing quality

India and China continue to be the chosen destinations for a pharmal industry hungry to lower research, development and manufacturing costs without sacrificing quality -

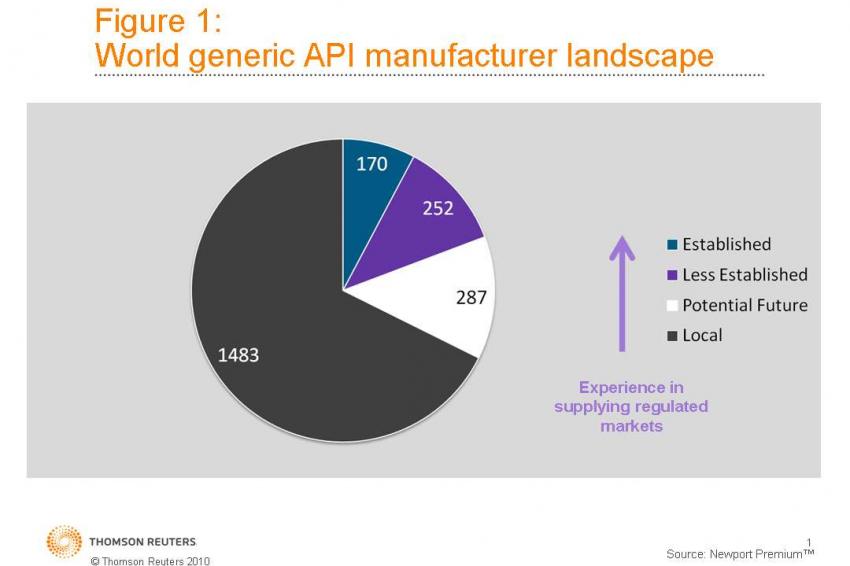

Figure 1

Figure 1 -

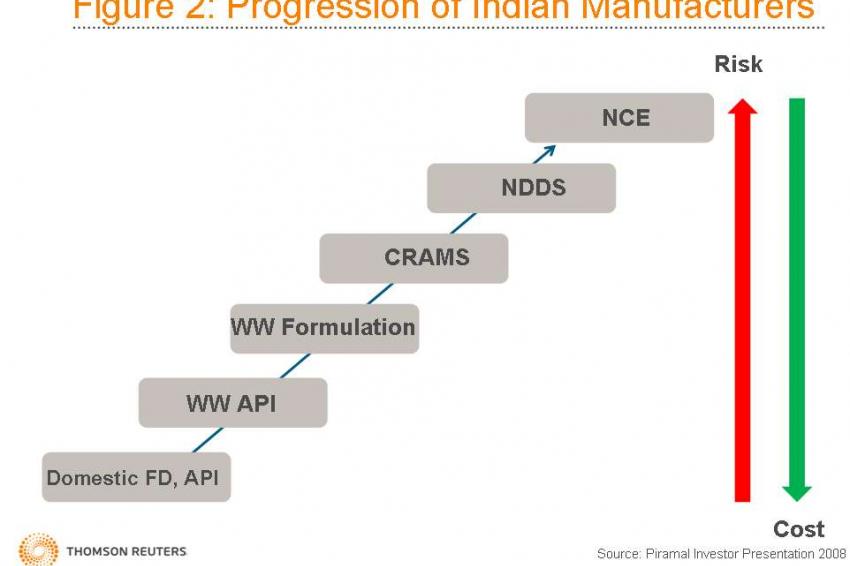

Figure 2

Figure 2 -

Figure 3

Figure 3 -

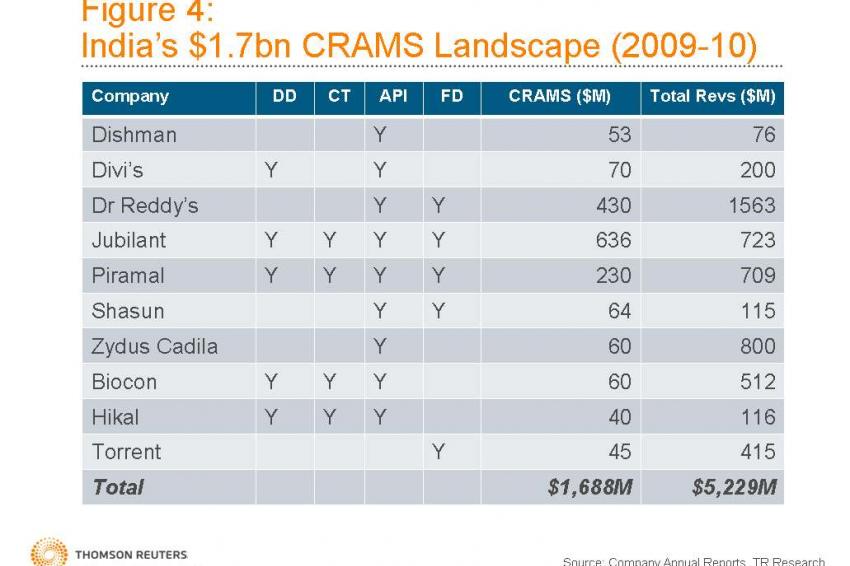

Figure 4

Figure 4 -

Figure 5

Figure 5 -

Figure 6

Figure 6

India and China are being discovered by more companies as ideal place for pharma sourcing. These two countries continue to be the chosen destinations for a pharmaceutical industry hungry to lower research, development and manufacturing costs without sacrificing quality. While the growth of clinical research and other contract development services in India and China has tended to occupy the news headlines, the most significant part of this growing industry involves the manufacturing of active pharmaceutical ingredients (API) and finished drugs (FD).

How have Indian and Chinese companies developed their businesses to cater to these new opportunities, what are their capacities to continue to expand services offered to highly regulated markets and what is likely to happen in the future?

The Current World Pharmaceutical Climate

According to IMS Health, the future growth expectations for world pharmaceutical markets vary widely from modestly growing to small declines in the highly regulated markets of the US, Europe and Japan to in excess of 10% in less regulated, emerging markets like India, China, Russia and Brazil. Big Pharma continues to consolidate and produce few new product launches while at the same time having to prepare for a large number of "blockbuster" patent expiries over the next few years. The business environment is equally challenging for generic pharmaceutical companies who face increasing competition from producers in lower cost countries like India, extreme price pressures in the major markets of the US and Europe, and for whom the promise of biosimilars is still some years from coming to fruition.

Despite these pressures, at around $66 billion at the end of 2010, the global pharmaceutical manufacturing market is growing strongly at around 13 to 14% according to CIBC. Of that spending, nearly 70%, occurs in-house, with the remainder coming from outsourced FD ($7 billion) and outsourced API ($11.5 billion) manufacturing. In a recent report by consultants Frost & Sullivan, global API market revenues are expected to grow by a steady 5% to reach $100 billion by 2013. In terms of API consumption, some 60% is still for captive use, with roughly 20% each going to the generic merchant and brand merchant markets according to the Italian industry organization Chemical Pharmaceutical Generic Association (CPA).

The Global API Manufacturing Landscape

During the past decade, Thomson Reuters has rated the capabilities of API manufacturers worldwide according to a series of objective measures that indicate their relative skill and experience in supplying highly regulated markets of North America, Europe and Japan. Measures contributing to the rating include regulatory filings made by companies in major markets, plant inspections made by regulatory agencies and demonstrated ability to support patent challenges, in addition to additional information gleaned from primary research activities.

These ratings range from Established (much experience over a long period of time), though Less Established (a good deal of experience over time) to Potential Future (little experience, or some gained only recently). A final rating of Local applies to companies with no demonstrated experience in working with highly regulated markets. It's also important to bear in mind that these ratings are not a pronouncement on the quality of the material produced by the companies, merely a gauge of their experience and ability to work in highly regulated markets.

Figure 1 shows that the vast majority of the world's manufacturers are at Local or Potential Future rating, which leaves 422 companies or less than 25% of the global industry with a demonstrable capability to supply highly regulated markets. Of those 422 companies, almost half are vertically integrated, meaning that they also produce finished products, and more than 60% of those companies are located in India, China, Italy or the US. Access to such a concentrated and relatively small segment of highly experienced API manufacturers has been one of the major drivers for consolidation in the generic industry over the past decade where today 9 out of the top 10 companies are vertically integrated and where many major acquisitions have been focused on acquiring API plants.

The Indian Industry in Detail

Now the 13th largest pharmaceutical market in the world according to IMS Health, India is home to many API manufacturers, contract services providers and finished dose producers. According to some estimates from the Indian government, India produces between 20 and 25% of the world's generic drug supplies and exported more than $8.5 billion of pharmaceutical products in 2009, $1.7 billion of which was API.

The significant cost advantages, concentration and proximity of raw materials, and manufacturing capacity coupled with better capital efficiencies and a rich pool of chemists and pharmacists have made India a natural destination for outsourced pharmaceutical research and manufacturing in recent years. It's useful to reflect on the development of this industry and capability that has been in progress for at least a decade.

Figure 2 shows the typical strategic path traversed by most Indian producers who have expanded quickly from domestic API production to supplying finished drugs on a worldwide basis. From there, many have been able to develop and offer contract research and manufacturing services (CRAMS), and a few have progressed as far as being able to develop their own novel drug delivery systems (NDDS) and innovative new chemical entities (NCE). As an example of just this transition kind of transition can been seen with Jubilant Organosys, which went from a base of producing pyridine chemicals and derivatives in the 1990s to a fully fledged pharmaceutical organization offering API production, finished dose form manufacturing and diverse contract services.

Much of the Indian API industry remains focused on domestic production or works with unregulated markets. Of the nearly 600 Indian API manufacturing groups tracked by Thomson Reuters, 442 of them are rated Local while only 67 have demonstrated long-term experience in working with more highly regulated markets (Established or Less Established). India has 89 companies with a Potential Future rating, indicating that there is a large class of companies that will continue to develop their capabilities and join the ranks of the Less Established and Established companies in the coming years.

The strength of the outwardly focused segment of the Indian industry can be seen through the lens of many regulatory measures. Filings of U.S .Drug Master Files (DMF) by Indian companies have risen almost exponentially from just 20 in 1999 to more than 285 in 2009, and the number of Abbreviated New Drug Applications approved by the U.S. Food and Drug Administration (FDA) that were submitted by Indian companies rose from a handful in 1999 to 142 in 2009. The Indian industry makes an equally strong showing in similar measures in Europe and other major regulated markets.

Not surprisingly, the development of this powerful industry has lead to a steady growth of its ability to offer contract services to companies elsewhere. According to the Indian Pharma Alliance, the Indian CRAMS industry is projected to grow to more than $2.5 billion in 2010, 50% of which will come from the contract manufacturing of APIs, 25% from drug discovery services and 25% from contract clinical trials work. Together CRAMS is likely to represent some 10% of all Indian pharmaceutical revenues very soon.

The Indian CRAMS business is dominated by Jubilant, Dr. Reddy's and Piramal but there are many other smaller and mid-size companies that now see significant revenues from this part of their business. The development of this contracting business has also spawned nearly 50 M&A deals totaling nearly $900 million of investment over the past few years and today, Indian CRAMS providers are working with partners as diverse as Amgen, Pfizer, Novo Nordisk and Nycomed on major long-term projects.

The Chinese Industry in Detail

China has also received considerable attention from Western companies looking to offshore pharmaceutical research and manufacturing. China is currently the 9th largest pharmaceutical market in the world at $12 billion according to IMS Health, and is projected to grow at between 12 and 15% during the next few years, a figure that is likely to make China the 3rd largest market by 2011-12. The China Pharma Review reported that the domestic API market is worth some $31 billion and Chinese manufacturers exported nearly $17 billion of APIs and $2 billion of finished dose forms in 2009.

Like India, the low costs, large capacity and talented base of scientists and engineers has been a major attraction, and improved protections for intellectual property have also helped drive the growth of the Chinese industry considerably in recent years.

Of the nearly 950 Chinese API manufacturing groups being tracked by Thomson Reuters, almost two thirds (603) are rated as Local. 143 are in the Potential Future tier and a mere 37 are either Established or Less Established, or about half that of India. The contrast between the capability and experience of the Indian and Chinese industries to serve highly regulated markets is further shown by Figure 5 where Chinese companies best their Indian rivals in Japanese DMF filings only. Like India, the large number of companies at Potential Future rating also suggests that their industry still has plenty of room to develop and expand its capability to supply highly regulated markets.

While China boasts nearly 1,300 finished dose manufacturers, there are only 3 companies holding U.S. Abbreviated New Drug Application (ANDAs) in comparison to nearly 30 Indian companies. On closer examination, it's also interesting to note that these Chinese-held ANDAs were in fact all acquired from US manufacturers, are therefore not Chinese-developed generic products, and a number of those products are discontinued in the US. However, as Figure 6 shows, there are now many Chinese companies working on contract with both major innovators and generics and it is very likely that new ANDAs will soon be approved for more Chinese companies.

The Future Outlook for Pharma Sourcing from India and China

Many Indian companies continue to shift their attentions away from API supply and towards more lucrative finished products and value-added CRAMS business. While this will certainly fuel continued healthy growth in outsource work for Indian companies, it is also likely to create an opportunity for more capable Chinese API manufacturers to fill the increased demand. Chinese companies are also likely to gain from the increased sourcing of advanced intermediates by Indian companies no longer able to, or interested in, producing these complex chemicals as their businesses move away from API production altogether or focus on performing final synthesis steps only.

While today, most discussion of API sourcing is usually focused on small (chemical) molecules, it's important to note that Indian and Chinese companies are also very active in manufacturing biologic drugs. While the quality and testing of these drugs may not yet meet the needs of major market biosimilar regulations, certainly for supply to their domestic, in addition to less regulated and unregulated markets, China and India are likely to be major destinations for supply of copy-biologic drugs too.

As regards the development of the Chinese outsource business, the effects of strengthened State Food and Drugs Administration (SFDA) oversight, more stringent EHS regulations and enforcement, coupled with increasing labor costs is raising costs. Smaller and less capable companies will fall by the wayside or be acquired by stronger firms who will then have the financial muscle to compete to supply more regulated markets. However, the extent to which Chinese companies enter highly regulated markets in significant numbers is likely to be strongly influenced by the growth of their domestic market. For many companies, it may be a far less costly and less risky proposition to compete in a strongly growing domestic market rather than to acquire the skills, knowledge and experience to compete with established players in highly regulated markets.

But whatever the outcomes, simply for reasons of cost containment, sourcing from China and India will continue to be a dominant theme of the pharmaceutical industry throughout this decade and there is plenty to suggest that there is a strong and capable industry in both countries that are eager to address this growing demand.

Contact

Thomson Reuters

215 Commercial Str.

Portland, Maine 04101

+1 207 8719700

+1 207 8719800