The Pharmaceutical Industry On The Move

Lessons to be Learned from the Chemical Industry

-

The pharma industry is in need of change. What is happening to an industry that still enjoys high margins? ((C) Fotolia/Danomyte)

The pharma industry is in need of change. What is happening to an industry that still enjoys high margins? ((C) Fotolia/Danomyte) -

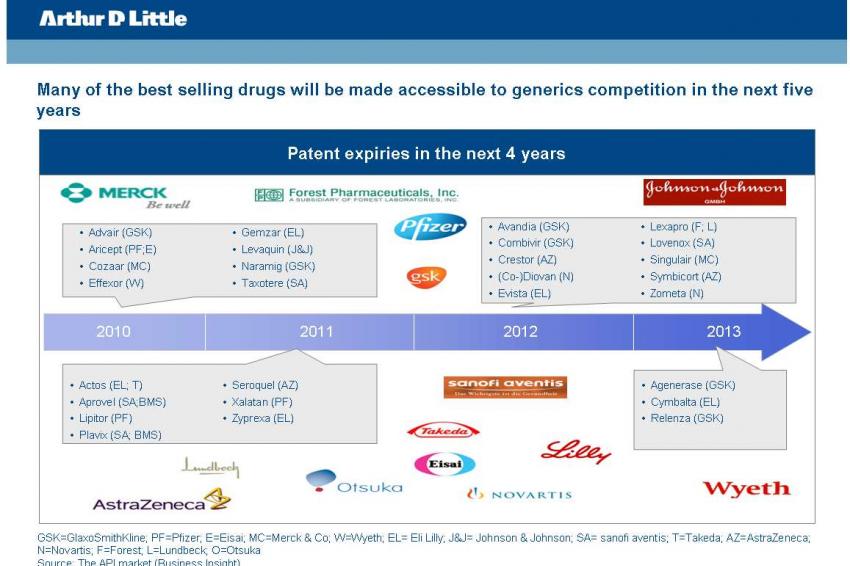

Figure 1

Figure 1 -

Figure 2

Figure 2 -

Figure 3

Figure 3 -

Figure 4

Figure 4 -

Figure 5

Figure 5

Shifting Priorities - Our world is faced with a growing and aging population. In developed countries, people search for wellness, while in emerging economies, populations seek better conditions of life. The development of BRIC countries, especially BIC, is leading to huge new markets. All this is triggering growth in the health and nutrition sector.

Nevertheless, the industry seems to envisage the opposite. The $780 billion global market is on the move and so are their key players - and they are suffering.

In the last half of 2010, several announcements were made by Roche, Novartis and Bayer. They all send the same message: cutting manpower, costs and searching for higher efficiency. But this is only the tip of the iceberg. In the last years, Pfizer has laid off more than 30,000 employees, GlaxoSmithKline more than 10,000, Merck around 23,000, while AstraZeneca is close to 20,000 less employees due to restructuring and optimization programs.

So what is happening to an industry that still enjoys high margins?

The growth engine has slowed down from 9% per year in the last decade to slightly above gross domestic product (GDP) levels. This provokes a deterioration of top line growth that will have an increasing impact on margins if costs and services are not adapted. At the same time, a number of patent-protected blockbusters are set to expire in nearly every global pharmaceutical company. Moreover, R&D has doubled since 2000, while the number of new drugs remains at a constant level over the last few years.

Patent expiries in attractive blockbusters have triggered the strong, double digit annual growth of generics. Today, the highest growth of Drug Master File (DMF) submissions - as an indicator of changing markets - already comes from India. It is followed by the U.S. for DMFs of generic active pharmaceutical ingredients (APIs) - in other words, a commoditization is taking place in traditional markets, and competition is rising in developing countries. Furthermore, the market is rapidly changing from a supplier to a buyer market. All of this will have an additional impact on margins going forward. Today, the pharmaceutical industry does not seem to be prepared for this: A plant utilization rate of 50-60% is a true indicator for the current effectiveness of this industry.

Learning From the Specialty Chemicals Industry

All these threats have been seen in another industry: specialty chemicals, often considered the historic root of the pharmaceutical industry. It was during the first oil crisis in the 1970s that the petrochemical industry awoke and started a long journey to efficiency. History repeated itself with slightly different mechanisms when specialty and fine chemicals were threatened by cheap imports from China and India in the late 1990s. The industry has learned its lessons, but over a long and suffering journey paved with mistakes.

For years, companies in the specialty chemicals industry believed that all solutions to globalization and rising competition in the East, especially from China, could be answered with better technology, new products and a stronger focus on more services to win the battle.

It took time for the industry to understand that the problems could only be solved by changing the business model towards a more market centric model ("What do you need?"). This went hand-in- hand with the experience that, in many markets, it was sufficient to provide offerings of "good enough quality." Many companies had to learn the hard way that some specialties have been commoditized, that services do not pay off a premium and that the cost structures have to consequently be adapted significantly.

Furthermore, the number of true specialties that can afford high costs has not increased since the mid 1990s. The industry needed to learn to live with decreased top- and even bottom lines between 1998 and 2006 - for which the whole process chain had to be adapted.

The cost optimization cycle started by improving the production processes, followed by site closures and a shift of production to other regions. Much time and money was wasted by incremental optimizations in one part of the process chain (e.g. production). However, in 2004 it became obvious that a more comprehensive approach, covering many parts of the process chain with measures from different areas that tie into each other, was needed to produce a step change in costs.

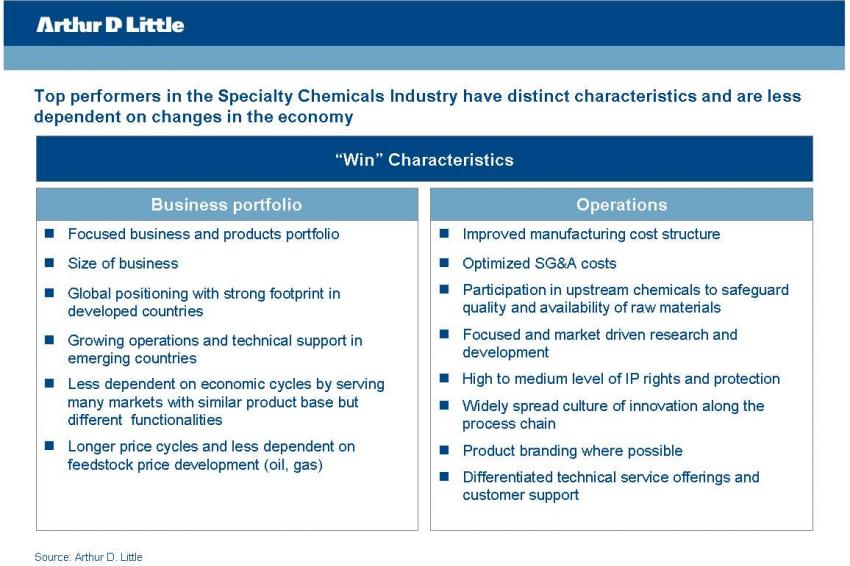

A perfect indicator for sustainable improvements is selling, general & administrative expense (SG&A) costs: They will only drop and remain at a lower level if many parts of the process chain are optimized simultaneously. A recent study by Arthur D. Little shows that this process is not finalized, and many chemical companies are still struggling with a multi-step approach for operational improvements.

A key element of success is the focus on core competencies that fit to well-understood markets and customers, and the reduction of complexity of products and processes at all levels. Iterative improvements have only lead to partial optimizations in the profit and loss (P&L), which have not been sustainable over more than two to three years.

It took roughly a decade for the industry to change its way. A lot of approaches have been tried and tested but capital efficiency - a clear indicator of success - remained below average for a long time.

Challenges Going Forward

Today, the pharmaceutical industry is confronted with most of the challenges the specialty chemicals industry has dealt with in the last decade - namely, a business active in different markets, with many different products. It is looking for answers in a changing environment. And the business models that proved to be right for many years seem incapable of tackling the challenges of the future.

There are several key challenge areas for the pharmaceutical industry through 2020 (fig. 1).

Each challenge offers opportunities, but also presents multiple issues to be tackled. Some pharmaceutical companies have already started to optimize certain areas. What is often missing is a holistic approach, which might end up in new business models and different ways to operate.

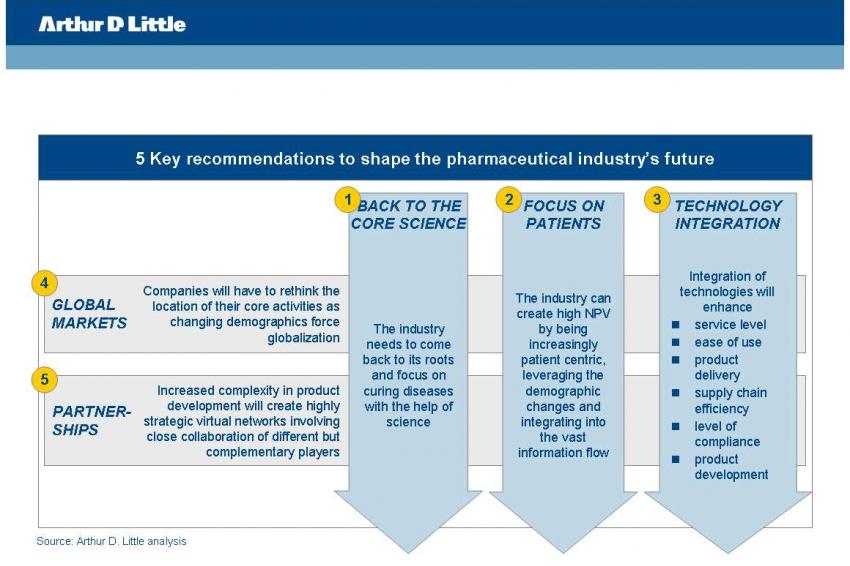

First of all, the business model has to be revised. Five key recommendations will change the landscape of approaching the market (fig. 2).

This will lead to a change from the historic "finding the molecule and market it" model (product centric approach) to an approach which is back to the roots of "identifying the need and use science, technologies and networks to answer it" (market centric approach). This also implies that companies have to rethink the location of their core activities, because changing demographics are forcing globalization.

For the pharma industry, it will not be sufficient to use a step-by-step approach or to optimize parts of the process chain. A holistic approach, with multiple measures starting in R&D and ending with different skills and approaches, will be needed in order to maintain market share and profitability.

It is of interest to learn how the specialty chemicals industry discovered the answers: Changing business models required well-elaborated and realistic change concepts and a carefully designed holistic implementation in order to reach new horizons.

Why would the pharmaceutical industry repeat mistakes and waste resources, when the answers can be found just across the fence?

Key Drivers In Evolution Towards A Global Pharmaceutical Industry 2020

Market

• Growth in the global pharmaceutical market is expected to slow down to 3% a year

• Pharmaceutical companies struggle to maintain both growth and profitability as margins decrease

• Pharma growth is now driven by emerging countries, reorganizing geographic priorities for the industry

• As blockbuster products come to an end, niche marketing becomes ever more important

Regulation

• The global debate on patents fuels political pressures and incentives which pave the way for generics

• Limitation of available funds leads to price pressure

• Attention in healthcare is shifting towards prevention

• New regulations limit access to and interaction with prescribers

Technological

• Innovation becomes more complex; despite continuing R&D spend, new drug approvals are lagging

• A global wave of partnership formation is taking place

• Rapid growth of biotech leads to increasing share and value of biologics

• Increased technology integration

Science

• Prescriber access is more and more challenged as focus on patient centrism is growing

• Key target patient groups are changing with demographic evolutions (e.g. aging population)

• Higher pandemic risks lead to an increased importance of vaccines

Source: Trends in pharma and prioritization (outlook 2020), Arthur D. Little analysis

Contact

Arthur D. Little GmbH

Gustav-Stresemann-Ring 1

65189 Wiesbaden

Germany

+49 611 7148 0

+49 611 7148 290