Complexity Within Biosimilars

Gold Mine or a Dead-end for the Generic Industry?

-

-

-

Peter Wittner, Interpharm Consultancy

Peter Wittner, Interpharm Consultancy

Hard to Copy - Market data shows that sales of biotech products are worth billions of dollars worldwide - just the sort of prospect that normally brings generic manufacturers rushing in to take advantage. Usually, patent expiry is followed by a flood of low cost generics that lead to prices falling by 80-90%, but this has not happened yet with biological products. Why not?

It is partly due to the great complexity of the products and the difficulties in copying them accurately. In addition, Europe has set high regulatory standards for proving equivalence and the U.S. has only recently created legislation for a biosimilars pathway.

The Potential Market

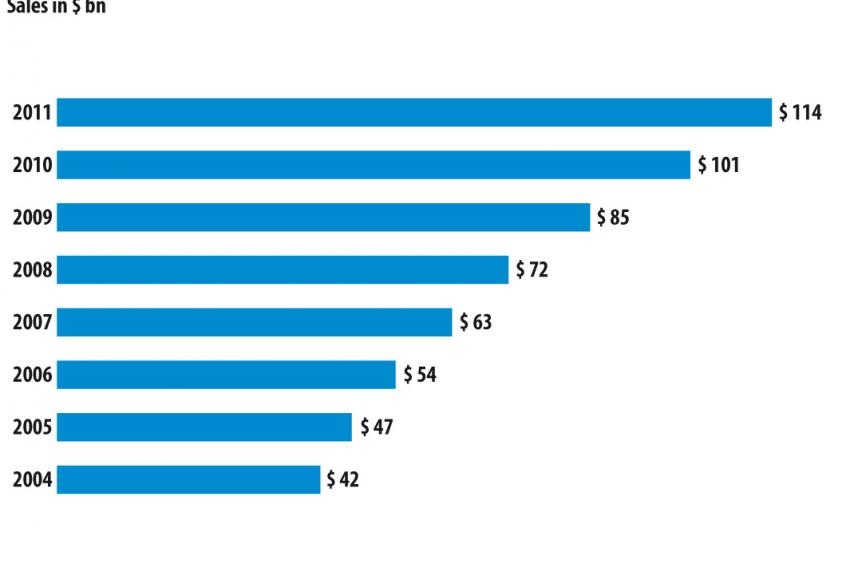

Estimates suggest that sales of Biological product in 2010 will exceed $100 billion worldwide with over $60 billion of that coming from the U.S. alone. Fig. 1, based on figures from a presentation at the Biosimilars India conference in 2009, demonstrates that this could grow by 10% in 2011.

While many of these products still benefit from patent protection, several others have lost exclusivity in Europe and the normal pattern is for patent expiry to be the trigger for a flood of copies to hit the market with the almost inevitable plunge in prices, but this has not happened yet. Where there have been copies they have struggled to gain market share (fig. 2).

As an example erythropoietin lost patent cover in the EU in 2007, but still they had worldwide sales of $5 billion in 2009. In the past, generic companies have happily copied products with much smaller turnovers - so what is different here?

The Problem With Biosimilars - Equivalence

Biosimilars are very different animals from small molecule generics. Their enormous size brings with it much greater complexity and thus a much bigger headache for generic companies trying to prove that their copy is similar to the original. Atorvastatin, for example, had a molecular weight of around 500 whereas a product like Peginterferon has a weight in the region of 40,000.

With small molecule generics, a simple bioequivalence study on about 24 volunteers is generally adequate to convince the regulator of the product's equivalence to the original. In regulated markets, this is not enough for biologicals; the regulators want to see a package of clinical studies to demonstrate that the copy is sufficiently similar to the original to be used for the same indications.

Another barrier to overcome concerns is immunogenicity. Companies registering biosimilars have to demonstrate to the regulators not only that their product works in the same indications as the original, but also that it is just as safe and no more likely to cause an immunological response than the original.

The problem of demonstrating equivalence is a real issue in European countries and the other regulated markets that have copied the European Medicines Agency's (EMEA) approach to biosimilars. The EMEA started issuing guidelines for biosimilars in general in 2006 and has added specific substance guidelines over the years since then. As a result, there are several copies based on filgrastim, erythropoietin and somatropin available in Europe, but this is far from the dozens of copies that normally flood into the market for other products.

The situation is worse in the U.S., where no such guidelines yet exist, although the enabling legislation has finally been passed. Until now, though, companies have needed to create virtually a complete copy of the originator's regulatory documentation so that only a handful of biosimilar products have reached the market.

In less regulated parts of the world, however, the market has opened up more with an abundance of biosimilars available. Biosimilars are often bought on tender and used in place of the product that was previously supplied. There appears to be frequent substitution due to the lower regulatory barriers and the acceptance that originals and Biosimilars can be interchangeable.

Interchangeability

It is this issue of interchangeability that has proved a major barrier to biosimilars in Europe and is likely to do the same in the U.S .when the regulatory pathway is in place. Put simply as an equation reflecting the mindset of the regulators:

For small-molecule generics: A = B

For biosimilars: A ≠ B

What this means in practice is that the European regulators have stated that the grant of a marketing authorization to a biosimilar does not mean that it is interchangeable with the original, rather it is merely sufficiently similar to be used as an alternative. As a result, prescribers are reluctant to switch a patient from the original brand on to the copy, despite any possible cost savings. In addition, most EU countries have specified that biosimilars should be prescribed by brand name rather than an International Nonproprietary Names (INN) chemical name, thereby precluding the possibility of switching or substitution by the pharmacist.

What appears to be happening instead is that prescribers in European countries are tending to only use a biosimilar product on a newly diagnosed patient. This acts as a very effective barrier to deeper market penetration, as the substitution that is the norm with standard generics is just not happening. As a result, biosimilars seem to have only taken a few percent of the market so far.

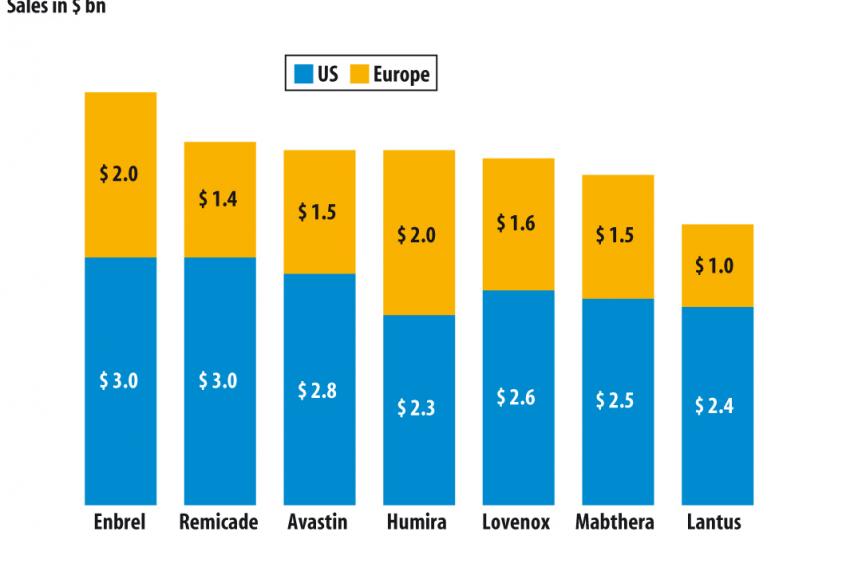

The significance of this barrier is that most of the sales of biological products take place in those relatively high-priced EU and U.S. markets where the barriers exist. Consider fig. 3, which shows

the breakdown of sales of leading biological products. Since worldwide sales of Enbrel amounted to $6.6 billion, these two zones account for 75% of world sales. Similarly for Remicade, sales worldwide total $5.9 billion so that here, too, the EU and U.S. accounted for 75% of the world total.

When biosimilars start to reach the U.S. market in significant numbers, and this is dependent on the FDA creating a mechanism and guidelines, it is quite probable that the same mentality that prevails in Europe will be the case in the US.

This is why companies selling biosmilars really need to find a way to overcome the interchangeability issues in both the EU and the U.S. The new U.S. legislation provides guidance on what is required to prove equivalence rather than just similarity, but only time will tell whether the FDA ever accepts a copy as being 100% identical to the original and thus interchangeable.

Contact

Interpharm Consultancy

55 Northiam, Woodside Park

London, N12 7JH

+44 20 84465572

+44 20 84465572