Bayer Presents Monsanto Takeover Plan

24.05.2016 -

-

(c) Bayer AG

(c) Bayer AG -

-

The Bayer CEO Werner Baumann said “this transaction is the next logical step to drive our Life Science focus and an opportunity to create a global leader in the agricultural industry able to advance the next generation of farming.” In a nutshell, Baumann said, a combination with Monsanto would “reinforce Bayer as a global innovation-driven life science company with leadership positions in its core segments.”

The Bayer CEO Werner Baumann said “this transaction is the next logical step to drive our Life Science focus and an opportunity to create a global leader in the agricultural industry able to advance the next generation of farming.” In a nutshell, Baumann said, a combination with Monsanto would “reinforce Bayer as a global innovation-driven life science company with leadership positions in its core segments.” -

(c) Bayer AG

(c) Bayer AG -

(c) Bayer AG

(c) Bayer AG -

(c) Bayer AG

(c) Bayer AG

Bayer has moved quickly to deflect criticism of its proposed acquisition of Monsanto, and possibly hasten the US company’s response to its offer, by publicly laying all terms and conditions on the table. Since news of the proposed deal broke on May 19, the Bayer share has continued to plunge. Monsanto’s share has also lost ground.

In a conference call with journalists to discuss the plans, the Leverkusen, Germany-based former chemical giant now fully focused on life sciences said its offer for the US player is worth $62 billion or $122 per share.

The all-cash proposal, it added, represents a 37% to Monsanto’s share price of $89.03 on May 9, 2016 – the day before its written offer was sent– and a 16-fold premium to Monsanto’s earnings before the unsolicited bid was announced.

From a financial perspective, criticism of the deal up to now has focused on the expected high cost and the level of debt it could conceivably require. From an ethical and environmental viewpoint, attention also has focused on Bayer’s potential embrace of genetically engineered seed and crops, the mainstay of the US competitor’s business activity but unpopular in Europe.

Bayer’s CEO Werner Baumann, its chief financial officer, Johannes Dietsch, and Liam Condon, president of the CropScience segment, told journalists the planned acquisition is “strategically compelling and completely logical,” while at the same time seeking to underline Bayer’s position with facts and figures published for the first time since the plans became public.

The German company also presented a letter written on May 10 to Monsanto’s board of directors to discuss the bid. In it, management confirmed the talking points Baumann said had already been put forward to the US rival.

All in all, Bayer said it has concluded that a combination of the two businesses makes better sense than the strategic cooperation alternatives discussed with Monsanto – and other industry players – in past years, especially in view of the need to find solutions for the challenges presented by a growing global population including a warming climate and a shortage of water.

From Bayer’s perspective, the CEO said “this transaction is the next logical step to drive our Life Science focus and an opportunity to create a global leader in the agricultural industry able to advance the next generation of farming.” In a nutshell, Baumann said, a combination with Monsanto would “reinforce Bayer as a global innovation-driven life science company with leadership positions in its core segments.”

As advantages for the combined company, he pointed to cost synergies of $1.5 billion after three years, plus additional integrated offer benefits in future years and a “compelling value-creation potential.” Here, core EPS accretion by a mid-single digit percentage is foreseen in the first full year after closing and a double-digit percentage thereafter. Among other benefits, Baumann named strong free cash flow generation, which he said would enable “rapid deleveraging post-acquisition.”

The CEO said the proposed merger would create a company with life science sales totaling more than €81 billion, including the consumer health business acquired from US-based Merck & Co in 2014 and the animal health business (which Bayer is widely expected to divest to help finance the Monsanto acquisition).

As of May 23, Monsanto had not yet commented on the unsolicited offer. Earlier, the US company said it would not do so until it had completely analyzed all aspects of the proposed transaction. In its now published letter to the US seeds giant’s board of directors, Bayer said a merger would bring together the two sides’ leading Seeds & Traits, Crop Protection, Biologics and Digital Farming platforms. More specifically, it would profit from Monsanto’s leadership in Seeds & Traits and Bayer’s broad Crop Protection product line across a comprehensive range of indications and crops.

From a geographic perspective, Bayer said the “truly complementary” combination would significantly expand the German player’s own long-standing presence in the Americas as well as its position in Europe and Asia/Pacific and that “customers of both companies would benefit from the broad product portfolio and the deep R&D pipeline.”

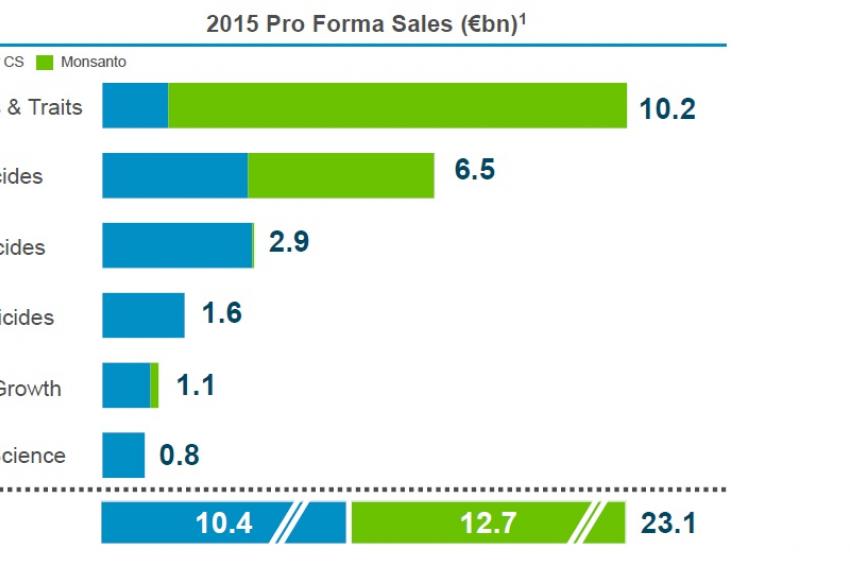

As part of its online presentation at https://www.advancingtogether.com/en/home Bayer drew the shape of the global agricultural chemicals sector in a post-merger world with pro forma figures showing that the combination with Monsanto would produce a company with relevant sales of €23.1 billion, ahead of the combined Syngenta/ChemChina’s €14.8 billion. The ranking includes the prospective DowDuPont agriculture company with €14.6 billion as a close third and shows BASF bringing up the rear with €5.8 billion.

Bayer/Monsanto would be number one in Seeds & Traits, the presentation shows, thanks largely to the US company’s already leading position. The merged enterprise would have herbicide sales of €6.5 billion, with fungicides (€2.9 billion), insecticides (€1.6 billion), seed growth (€1.1 billion) and environmental science (€0.8 billion) accounting for the remainder.

North America, with revenues of €10.5 billion, would be the most important sales region by far, followed by Latin America (€5.8 billion), Europe (€4.7 billion) and Asia-Pacific (€2.1 billion).

None of the figures reflects divestments mandated for anti-trust reasons, but Bayer – in contrast to some analysts – believes that there will be few such issues as the portfolios are largely complementary.

Addressing financial arrangements, Bayer said that, based on advanced discussions with and support from its financing banks, BofA Merrill Lynch and Credit Suisse, the company is “highly confident in its ability to finance the transaction,” which would be put together through a combination of debt and equity. In addition to its legal advisors Sullivan & Cromwell LLP (M&A) and Allen & Overy LLP (Financing), Bayer has retained Rothschild as an additional financial advisor.

The would-be acquirer said it expects the equity portion of the deal to represent around 25% of the transaction’s enterprise value. This would be raised primarily via a rights offering (which critical investors previously said they fear would dilute the German company’s share value).

In its letter to Monsanto, Baumann told the company’s chairman and CEO, Hugh Grant, that Bayer has “long respected Monsanto’s business” and shares its vision to “create an integrated business that we believe is capable of generating substantial value for both companies’ shareholders."

He assured Monsanto additionally that “Bayer has a successful track record of working with global authorities to secure the necessary regulatory approvals and has extensive experience integrating acquisitions from a business, geographic, and cultural perspective.”

With the necessary analysis of all implications of a merger already completed, the German CEO said “Bayer is prepared to move expeditiously to complete customary due diligence, negotiate and execute a definitive transaction.” He declined to present a timetable for closing the deal, as he said this would depend on the timing of Monsanto’s response.

In response to criticism that a takeover of the US competitor would be too complex to be achieved smoothly, Baumann said the €17 billion purchase of German pharmaceutical producer Schering in 2006 was far more complex, especially as the Berlin drugmaker’s corporate structure was more complex than that of Monsanto.

As to whether combining with Monsanto would damage Bayer’s perceived positive reputation due to Monsanto’s negative public perception, both Baumann and Condon stressed that the German company would continue to adhere to the highest ethical standards as it has done in the past. Some observers have speculated that Bayer might abandon the Monsanto name after the purchase, just as it has dropped other brands following previous acquisitions, in this case helping to distance the new company from Monsanto’s reputation.

In dialog with journalists, Liam Condon said Bayer has proposed that the global Seeds & Traits and North American commercial headquarters be located at Monsanto’s home base of St. Louis, Missouri, USA, while the global Crop Protection and divisional Crop Science headquarters would remain at Monheim, Germany, with an important presence in Durham, North Carolina, USA, as well as many other worldwide locations. Digital Farming for the combined business would be based near San Francisco, California.