A New Century for Purchasing

Procurement in the Chemical, Pharmaceutical And Healthcare Industries

-

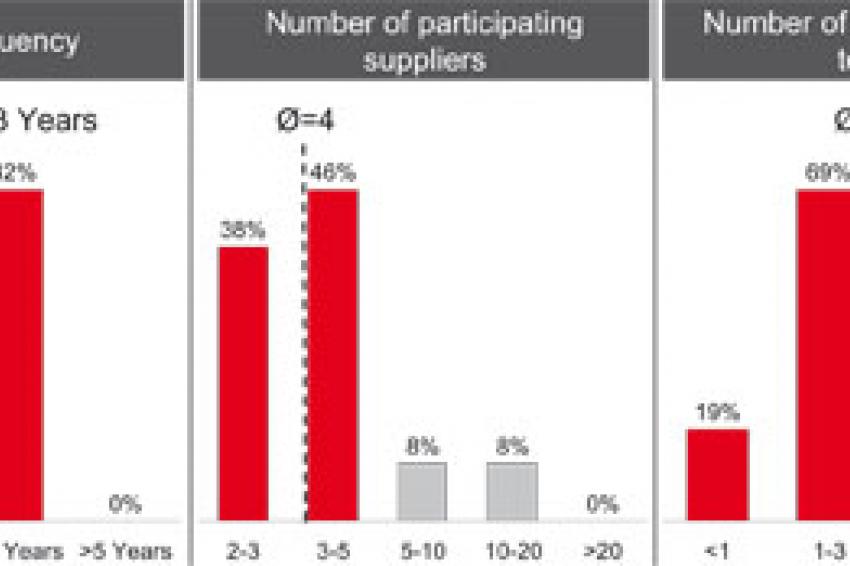

Fig. 1.: Tenders

Fig. 1.: Tenders -

Fig. 2:

Fig. 2: -

Fig. 3:

Fig. 3:

Status quo, quo vadis - Globalization, profound crises, new technological developments - these are the trends that are shaping business today. But where does procurement stand in light of these developments? Where is there potential and which trends must be urgently addressed? Consultancy Valueneer set out to answer these questions with its Global Procurement Study, in which more than 790 companies within all areas of industry from 62 countries participated.

Most companies in the chemical, pharmaceutical and healthcare industries are unable to implement available potential for cost reduction in procurement. Short-term potential - such as the financial crisis - is not being tapped. The main factor here is a lack of qualified employees in procurement; at the same time, strategically important positions remain unfilled.

Major Procurement Topics in Industry

In general, procurement in the chemical, pharmaceutical and healthcare industries has a strong operational focus. Price and offer analysis are of the highest priority, followed by demand forecast and analysis and management of supply shortages. Each of these areas of focus has an above-average relevance compared to other industries.

The most important strategic procurement topics are supplier evaluation, tendering and supplier qualification as well as searching for new suppliers. Compared to other industries, tendering in particular appears to be of particular importance for companies active in the chemical, pharmaceutical and healthcare industries. Meanwhile, the search for new suppliers has less importance attached to it; this means tendering is a standardized tool, but is not used as cost-effectively as possible.

Dominant Procurement Topics in the Industry

For day-to-day operations, the procurement department of most companies is well positioned. Observation of the dominant procurement topics shows that purchasing offices are seen as the place where orders are carried out and where supply is guaranteed.

However, when one looks into strategic procurement, a deviation can be observed. Only half of the working time that is considered to be optimal for strategic tasks is actually implemented in this area. While tendering has a higher priority in chemicals, pharmaceuticals and healthcare, less time is committed to this area. Accordingly, the qualified search for new suppliers also gets little attention on a day-to-day basis.

A closer look at the topic of tendering shows the following trend: Procurement departments do too little in this area relative to the total procurement volume, with few suppliers and, above all, with too few potential new suppliers.

This means that one of the most important measures for cost reduction in procurement - regular and broad tendering - is used insufficiently. This leads to unnecessarily high purchasing costs.

In almost 20% of the invitations to tender, no potential supplier is included; this negates the purpose of a tender and throws a considerable amount of savings out the window.

Measures to Take During a Crisis

Companies in the chemical, pharmaceutical and healthcare industries often have a hard time dealing with sudden changes in situations. Only 28% of the companies make use of new tenders -the most important lever - in order to take advantage of additional potential a financial crisis brings. Even with the support of existing suppliers, the companies in these industries are much more conservative than in other companies.

More than 60% of the analyzed chemical, pharmaceutical and healthcare companies instituted a temporary reduction of working hours, significantly more than in other industries. This resulted in less resources being available for important tasks.

Possible Contribution to Procurement Earnings

According to self-assessments conducted by purchasing managers, there is potential industry wide for cost reduction of an average of 10%. The financial crisis added another 6%. The short term turnover of just 2% of this potential is sobering. As far as the crisis is concerned, that means an unrealized potential of 4% remains.

Causes and Measures

One of the identified reasons for the poor implementation performance and the internal focus on the day-by-day business is the widespread organization of procurement under the chief operations officer (COO). This organization model is most common in the chemical, pharmaceutical and healthcare industries, with 63% in comparison to 42% in other industries.

A COO often focuses on maximal supply stability and does not see keeping procurement costs at a minimum as a main goal. This inevitably leads to performance disadvantages in this organizational model.

Procurement departments themselves in the chemicals, pharmaceuticals, health care have already recognized this. When asked which board member should ideally be responsible for the procurement department, nearly 80% of those active in purchasing said either the CEO or CFO.

Success Factor Personnel and Incentives

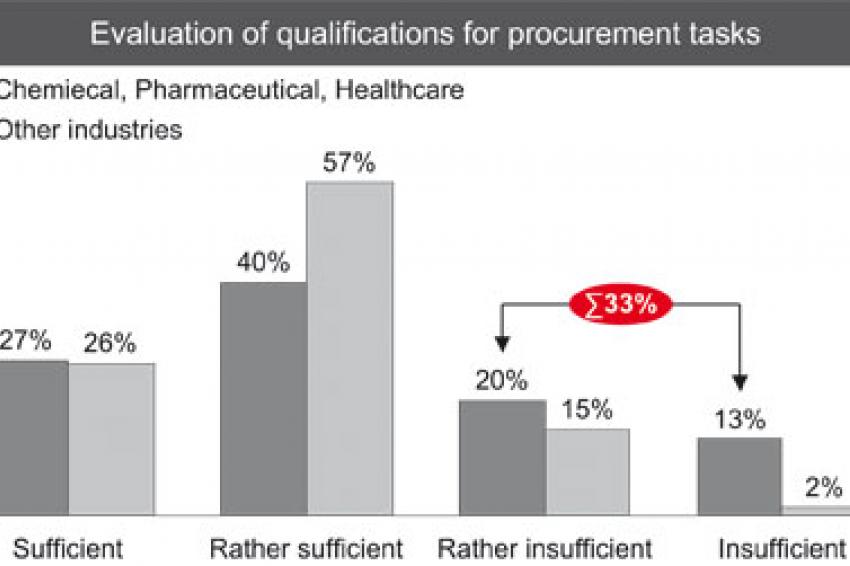

Success in purchasing cost reduction is only possible with a sufficient number of qualified employees; the study shows that this is exactly what is missing. Particularly alarming is that procurement managers are not usually able to raise top management's awareness of the lack of resources and skills.

Almost half the companies in the chemicals, pharmaceuticals, healthcare industries said they don't have enough purchasing staff. Furthermore, one third of the companies asked evaluate their employee's skill insufficient. While a good 60% of procurement personnel in chemical, pharmaceutical, healthcare companies have a university degree, this provides no advantage in this case. Rather, the highly qualified academic personnel are not able to implement their knowledge in the daily business. In general, the study shows that an optimal procurement department needs "the right mix" of theoretical and practical thinking personnel.

The lack of available and qualified personnel is further intensified by missing or insufficient incentives. Managers and staff in procurement benefit too little and too rarely from achieved cost savings - only 44% of the managers, well-fifth less than in other industries, and only 29% of employees benefit from savings achieved. The motivation is much lower than is the case for sales representatives.

Sourcing Markets

The trend toward global sourcing will also continue to increase for companies in the chemical, pharmaceutical and healthcare industries. The current sourcing markets in this sector are expected to change even more distinctly. The traditionally strong sourcing markets of North America and Western Europe are becoming less important; meanwhile, China remains the fastest growing region for the chemical, pharmaceutical and healthcare industries.

Conclusion and Outlook

While purchasing in many industries achieved first major successes by the evolving from a "simple" buyer into a value-added interface between the internal and external operations over the past two decades, this process has been neglected in chemical, pharmaceutical, healthcare industries. This is due to the lower purchasing cost share and the excessive-focus on security of supply. Due to these shortfalls, these industries are lagging behind in terms of strategy, organization, processes and potential realization.

Contact

ZLU Consulting und Management GmbH & Co. KG

Rotherstraße 8

10245 Berlin

Germany

+49 30 600501 0

+49 30 600501 118